Why companies stay private longer (SPL) and what it means for family offices as VC LPs

Part of Family Office Series

Companies are opting to stay private longer (SPL). 87% of US companies with revenues greater than $100 million are not traded on public stock exchanges such as NYSE or NASDAQ.

In this post, we examine some stats, potential reasons for SPL, and what it means for non-institutional investors.

Facts and Trends

6 vs 11 years: In 1980, the median age of a company at IPO was 6 years; by 2021, it was 11 years.

$100m vs $1.3b: In 1980, the median market value at IPO (inflation-adjusted) was $105 million; in 2021, it was $1.33 billion.

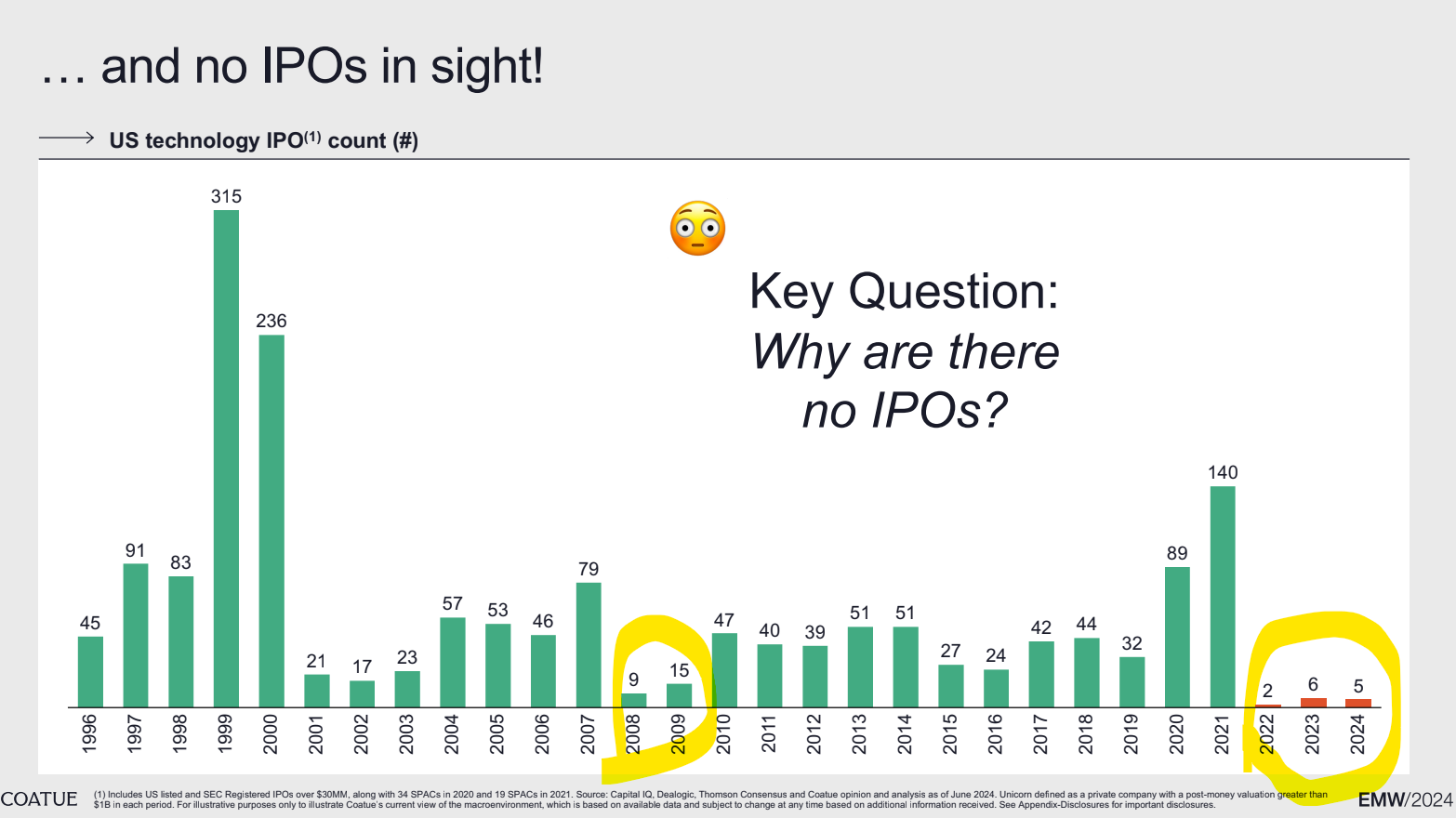

6.5k vs 3k: From 1980–2000, there were over 6,500 IPOs. From 2001–2022, fewer than 3,000—even with the 2021 frenzy.

The number of public companies in the US has fallen from 7,500 in 1997 to under 4,000 today, while the average age at IPO continues to rise. The result: the bulk of innovation and value creation is happening off the public markets, behind the velvet rope of private capital.

Why Are Companies Staying Private Longer?

Company Side

Regulatory burden: Sarbanes-Oxley and other rules have made public company life more expensive and distracting for management.

Abundant private capital: Private equity and venture funds now manage trillions in assets. In 2023, private equity funds managed $8.2 trillion, more than double 2018’s total. Companies like SpaceX, OpenAI, and Stripe have raised billions privately and reached valuations that would place them among the largest public companies—if they chose to list.

Control: Staying private allows founders and early investors to retain control, avoid quarterly earnings scrutiny, and focus on long-term strategy.

Market Side

Investment bank economics: IPOs are expensive—banks charge 7% fees on gross offering, though large deals sometimes negotiate down to 1–3%. For a $1 billion offering, that’s $21 million in fees.

Risk aversion: Banks used to underwrite (“firm commitment”) IPOs, taking on risk. Now, they’re more conservative, and direct listings or SPACs have emerged as alternatives.

Private market liquidity: The rise of secondary markets means early investors and employees can cash out before an IPO, reducing pressure to list.

What It Means for Investors

The implications are stark:

Missing the growth curve: The most explosive growth now happens before IPO. By the time companies go public, much of the upside has already accrued to private investors.

IPO risk: The data is sobering—80% of IPOs are unprofitable at debut, and two-thirds underperform the market within three years. Recent high-profile IPOs like Uber, SmileDirectClub, and Robinhood saw their shares fall sharply after listing, often never recovering to private market valuations.

Liquidity gap: With fewer IPOs and longer holding periods, public investors have less access to innovation and growth. Meanwhile, private market investors must navigate longer holding periods and more complex exit dynamics.

What It Means for VC LPs

For us, as allocators, this means adapting to a new reality. We see two scenarios:

Continuation of the SPL trend (80% probability): Private markets continue to dominate, with public markets becoming less accessible for new companies and investors seeking innovation.

Regulatory reversal (20% probability): A shift in regulation makes going public easier, swinging the pendulum back and opening the door for earlier IPOs.

Our strategy is shaped by these probabilities. The late-stage private and pre-IPO markets are crowded, expensive, and often deliver subpar returns for new entrants. Uber is a textbook case: by the time it went public, the exponential growth was over, and public investors bore the brunt of the risk while early investors had already cashed out.

“What seemed like a great opportunity to invest in a huge company turned out to be a case of getting on the elevator on the top floor.”

Therefore, we focus on the early stage, where value creation is greatest—but sourcing and access are the real challenges. We solve for this by investing as a fund of funds, partnering with specialist managers whose sole job is to find and back the best opportunities as early as possible.

The Evolving Private Market Playbook

Private markets themselves are evolving. The rise of the secondary market means that liquidity options are improving for early investors, founders, and employees—even as companies stay private longer. This is changing the venture capital model from “buy and hold” to active portfolio management, with secondaries and continuation funds now an essential part of the toolkit.

Meanwhile, LPs are increasing allocations to private markets, especially in technology and healthcare, and are seeking exposure through co-investments, secondaries, and sector-specific microfunds. The innovation supercycle—driven by AI and digital transformation—means the best opportunities will continue to emerge privately, not on the ticker tape.

The New Center of Gravity: Silicon Valley

This shift is part of a larger secular move away from traditional financial centers like New York and London toward Silicon Valley. Not only is the Valley the epicenter of company formation, but it’s also become the capital market for growth businesses. The culture, capital, and networks for scaling technology companies are all here, and the role of venture capital in driving innovation has never been more pronounced.

For family offices investing in VC funds, the path to top-tier opportunities increasingly runs through strong relationships and showing up! By pairing fund commitments with selective co-investments and SPVs, family offices can access high-conviction deals and deepen their exposure to innovation.

The key: build trusted networks with leading managers, stay disciplined in diligence, and bring your unique expertise or connections to the table. In today’s private market environment, those who are engaged, connected, and nimble will capture the best opportunities—well before they ever hit the public markets.

This is an educational post about GEX Ventures family office. It is for informational purposes only and may not be relied on as legal, tax, securities or investment advice and does not constitute an offer to buy or sell interest in any products offered by us or others. Email me at mk@gex.vc or leave a comment if you’d like to exchange ideas.

Agreed- the way FO LPs are allocating in private markets has strengthened, but access and network remains complex when seeking to invest in Tier-1. As a FoF investor, how are you avoiding thematic/vintage clustering and what are you prioritizing in your strategy?